Everyone wants to know when to pull their investments out of the stock market before a crash. If you know when the market will crash then you can make a ton of money off either liquidating your investments or simply shorting the market.

Predicting a stock market crash accurately is pretty easy. I am going to show you how professionals on the street predict stock market crashes and how they hedge their portfolio to generate additional capital along the way. In this article I am going to show you what variables analysts and portfolio managers look for to predict a stock market crash.

In order to accurately predict a stock market crash you need to understand what the difference is between an industrial and Malthusian economy, what causes them to grow, and what variables to look for to predict a crash. These variables are found by looking at the past 3 major stock market crashes in the U.S. Further, we look at how the market has evolved in relation to computer algorithms. Finally, at the end I summarize everything to give you a methodology to predict stock market crashes.

Here at Chronohistoria I teach people how to generate above average returns in investments (alpha). I do this so that everyone can have an equal shot at making money in the market. There is a lot of misinformation out there regarding markets and investments in general and I aim to correct some of that. I routinely publish articles on investment research, methodologies, and tips/tricks so that you are better armed to generate capital in the markets. Feel free to sign up for the free newsletter to remain up to date on everything investing.

Without wasting any time, let’s jump right into the article: How To Predict Stock Market Crashes

How The Stock Market Works

In order to predict a stock market crash we must first touch upon how the stock market works.

The stock market works by efficiently moving capital from bad investments to good investments. Over time this allocation of capital and wealth increases as businesses and companies become more profitable. Once an investment starts to perform poorly however investors will liquidate their positions and look for a better investment.

This is called the efficient market hypothesis. That markets are inherently efficient at allocating capital overtime. Burton G. Malkiel wrote a foundational article in 1987 that goes over this theory in extensive detail if you’re interested in reading it. (source)

Simply put, investors are looking to grow their capital in the fastest way possible. They do this by looking for investments that offer better returns than their previous investments.

So how does efficient market theory impact stock market crashes? The answer comes down to an increase in growth and risk present in all industrial economies.

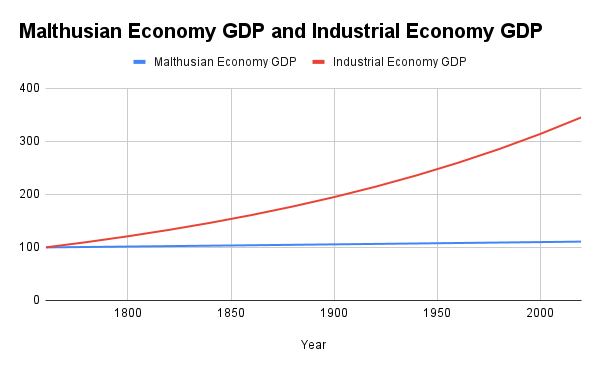

Market Risk In Industrial Economy vs. Malthusian Economy

Thomas Robert Malthus was an English cleric and economist that lived in the late 18th century. He is most widely known for his publication on the forecasting of human population variables and how this would impact overall economic growth.

This publication (An Essay on the Principle of Population) lays out how the future of the world’s economy was tied to overall land production worked by people. The underlying thesis is that there is only so much land to go around and eventually this would lead to famine which in turn would limit population, which would limit the total production capability of the land.

This is called the Malthusian trap. And it was the first prediction of a market crash.

However with the advent of the industrial revolution for the first time the market was moved outside of an agrarian economy and onto a production focused economy. This would be called the industrial economy and it resulted in an exponential increase in total wealth production.

However with this explosion in wealth production came an explosion in risk. In a Malthusian economy total risk present in the market is little to none. This is because the total value of the economy is based around the value of land which only increases over time (at a slow rate).

In an industrial economy the risk can go upwards of 100%. This is the underlying backbone of stock market crashes. It is very important that we understand this. In our current economic model we are no longer based around the value of land, but rather our economy is based around the value of production.

Why Can Industrial Economies Grow Faster Then Malthusian Economies?

The reason is simple, loans and the concept of credit. In a Malthusian based economy a bank or loan shark would know exactly how much revenue your plot of land returns per year. In an industrial economy however you can increase total return out of the same resources which increases total growth rate.

This means that in an industrial economy we start to see a rise in business loans and thus innovation. Simply put, if more people are willing to create businesses because they think they can develop, produce, and capitalize upon a trend then they will take out a business loan.

This means that in an industrial economy we see a huge rise in credit among the business elite. In turn this creates destabilization within the economy, which leads to market crashes. An increase in credit means that there is an increase in total risk in the overall stock market.

Simply put, if everyone is taking out loans to capitalize upon a trend we see massive innovation and risk increase in an industrial economy. Remember this as it’s important later on. What drives industrial economies is innovation, credit, and consumption all working in equal parts.

An example of this can be seen in the rise of more energy efficient machines in Germany, Japan, and the USA during the 20th century. From 1940 up through 1995 the most successful companies utilized cutting edge technologies to streamline factory production and grow a fledgling internet. Across the ‘developed’ economies of the world in the 19th century we see innovation, credit, and consumption all growing in relation to an increase in energy efficiency.

For those who are interested, in 2014 there was an article published in the New Journal of Physics that ties economic growth to an increase in energy efficiency within production. (Source here)

Stock Market Crashes Of The Past

In order to predict when our stock market will crash we need to look at the past. There have been three major stock market crashes over the past 100 years. The first was the stock market crash of 1929. Second was the 2008 recession. Finally the third was the 2020 pandemic.

We absolutely need to look at these previous crashes to find out what happened to the three variables that drive industrial economies. These are the variables of innovation, credit, and consumption. When one of these variables gets out of line then it can destabilize an industrial economy and cause a stock market crash.

The Stock Market Crash of 1929

In September of 1929 the U.S stock market started to decline. At first most people thought this was a temporary recession. This was because during the early 1920’s the concept of credit was introduced into the U.S economy. For the first time people could easily go out and buy a good on credit/loan that they would have to pay back in the future. (Source)

Sayings such as “Buy Now, Pay Later” became synonymous with the 1920’s. The problem however is just like all forms of loans eventually people would have to pay back what they borrowed. This overtime led to a massive debt crisis in the U.S. In the late 1920’s more and more people were attempting to emulate the rich and famous of society by living far above their means. (Source)

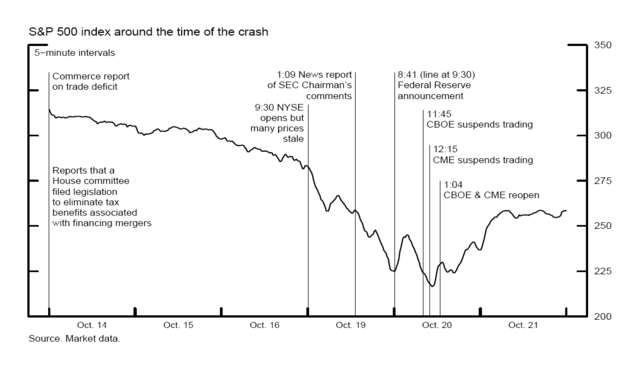

This all came to a head on October 24th when the entire U.S stock market fell by 11% in the first 30 minutes of trading. What happened over the next couple months was nothing short of panic selling which induced margin calls. Within a couple months the entire world’s market was down and innovation, credit, and production came to a standstill. The industrial economy had faltered.

The Three Variables in the 1929 Crash: Innovation, Credit, and Consumption

When looking at the crash of 1929 we need to analyze what happened to the 3 foundational models of an industrial economy. The reason why is because going forward the U.S economy implemented procedures that would protect from a similar stock market crash. By knowing these 3 variables we can better apply this situation to our contemporary market conditions.

Variable 1: Innovation

Leading up to the crash of 1929 innovation within the financial sector was massive. Almost every year another financial product or service comes out. These products and services allowed the U.S population to buy increasing amounts of goods and services on loan. (source)

In many ways the 1920’s U.S was the hotspot of the world’s innovation market. Companies from around the world were attempting to get into the U.S investor market to offer another good. This was because of the large growth in U.S industrialization during this time. (source)

Variable 2: Credit

The 1920’s saw what experts call a “credit crunch.” This is where all outstanding loans and revolving credit stops. At this point margin accounts are called and everyone must pay back what they owe.

The problem however is that when an entire economy is out on loan then we have a crash. Pre 1920’s administrations did not understand this and as such there were no policies in place to prevent consumers from taking out large loans consecutively. Further, banks during the 1920’s failed to update each other’s credit ledgers. (source)

What happened was a runaway credit system in which people constantly took out loans and set up the whole financial situation to fail.

Variable 3: Consumption

There must be a population that will consume enough of the country’s production to offset the expenses of production. Further this population must make enough to purchase the goods or services that a company produces.

During the 1920’s this consumption level rose faster than any other time period. More and more people were going out on loan to consume more goods than ever before. Further they had the ability to go out on credit to consume these goods.

However during the crash consumption came to a halt. People could no longer take credit for goods. (source)

What the 1929 Crash Teaches Us About Stock Market Crashes

During the 1920’s everyone in the United States was emulating the wealthy. Everyone was rich and famous, further everyone was using a new credit system to consume products. These products were created by companies who further went out on loans to expand their own product lines and increase production.

What we learn from this stock market crash is that whenever an industrial economy starts to see credit get out of line with production and consumption it will eventually lead to a stock market crash. For our time this means that if you see an increase in total loans/margin/credit within the economy then chances are a recession is coming up. If the market fails to correct fast enough then we will see a crash.

The 2008 Stock Market Crash

In the mid 90’s the U.S housing market started to explode. Administration after administration started to promote housing loans that would seek to expand the U.S housing market to more people. (Taxpayer relief act of 1997)

Now banks had the ability to issue loans to people who normally couldn’t make the payments on such a house. The trick here was that banks would bundle all of these loans together into something called “subprime” loans. These baskets of subprime loans would then be bought and sold among the banks who in turn would speculate on future economic conditions. (Source on the Glass-Steagall act repeal)

This led to a rapid destabilization of the U.S economy as banks were speculating on loan bundles which had both good and band mortgages in them. How the mortgage market works is if enough people start to foreclose on their homes then the banks will start to seize all properties to cover their losses.

With these subprime loans failing the industrial economy was set to collapse.

The Three Variables in the 2008 Crash: Innovation, Credit, and Consumption

The 2008 stock market crash changed the way that loans are dispersed throughout the United States. Further, it demonstrated that the financial sector within the United States could catastrophically fail. This sector failure caused the entire worlds economy to slip into a recession that took several years to get out of. (Article from 2010 that goes over the total global impact of the 2008 recession)

We need to look at how an imbalance of innovation, credit, and consumption led to the 2008 market crash. Coming out of the 2008 recession globalism became a dominant player and for the first time we as a world began to see just how quickly a stock market crash could impact the world’s economy.

Variable 1: Innovation

From the mid 90’s policy innovations led to an increase in affordable housing for all demographics within the United States. While these policies were directed at getting more people in houses it ultimately destabilized the U.S economy. (source)

This in turn caused a runaway effect where lenders would give out loans out to people who had bad credit just to sell a mortgage.

Simply put, innovation in financial products and policy allowed new types of loans. This in turn caused the housing market to explode as people started to buy their own homes.

Variable 2: Credit

Starting in the early 2000’s credit in the form of mortgage loans was out of control. People who couldn’t pay their mortgages were bundled together with those who could into credit packages. These credit packages were in turn bought and sold between financial institutions who in turn would speculate which ‘bundle’ of loans would pay out. (source)

This speculative fever overtime inflated the credit crisis. Bankers would profit from people taking out huge loans that they couldn’t pay back.

Credit availability for mortgages in the early 2000’s was all over the place. As such the entire housing sector in the U.S exploded. Investors were clambering to get in, which further increased speculation.

Variable 3: Consumption

The housing stock market crash of 2008 did not truly happen until people stopped consuming mortgage loans. When you have massive consumption in a sector which drives innovation and credit the total risk is high. It only takes a brief stop to the total consumption across the target demographic for the sector to crash.

Since 2008 markets have learned how to terrace consumption rates through inflation. However there is still a chance that consumption abruptly stops within a sector. If that stops then there is nothing that can be done and we will have a market crash.

Recent academic articles have looked at how consumption of high risk mortgage loans impacted the 2008 recession. This is cutting edge of economic analysis currently and I expect future academic papers to highlight how consumption risk is a driving factor of stock market crashes. (source for 2020 article in the American Economic Review that goes over mortgage consumption rates between 2006-2011 to highlight market crashes variance)

The 2020 Pandemic and Stock Market Crash

The 2008 housing market crash demonstrated how connected the world’s economy is. The 2020 pandemic demonstrated how susceptible the world’s economy is to consumption decline. (Source)

It is still too early to accurately talk about the cause and effects of the 2020 pandemic. However what is certain is that the stock market crashed in late February of 2020. This decline was caused by a global pandemic that forced countries to engage in a lockdown to prevent the spread across their population.

With a lockdown in effect worldwide all three variables came grinding to a halt. Innovation was at an all time low due to a missing labor force. Nobody was engaging in loans or the financial credit system. Consumption simply did not exist during the pandemic as the only thing people were buying was food and other essentials.

Further, people started to liquidate their holdings in stocks with a global supply chain and invest in domestic stocks such as natural gas, software, and healthcare. This caused a massive imbalance within global markets that reflected a growing isolationism policy across the world’s countries. (article going over these reflections in the S&P 500)

It’s too early to talk in detail about how each of the stock market crash variables were demonstrated in the 2020 crash. My estimate is that consumption was the first to decline as people quarantined, next innovation rates crashed as companies furloughed their workforce, last credit became riskier as risk of default increased. (source no credit default rates in Europe)

Again it’s simply too early to tell the full impacts of the 2020 pandemic. All that matters is that the 3 variables of market crashes were exhibited.

How Previous Stock Market Crashes Impact Modern Portfolio Management

This is very important to understand. Modern portfolio management utilizes past historical data to calculate total risk in a position. This includes previous market crashes and their variables.

With every single market crash good portfolio managers learn how to hedge their clients positions. This is done by incorporating historical variables that caused previous stock market crashes.

We need to look at how fast the market can crash now in order to predict a stock market crash in the future. There are two ‘flash crashes’ that I will outline. The flash crash of 1988 and the flash crash of 2010.

Flash Crash of 1988

Before the mid 1980’s this was done by hand with professional analysts calculating the total risk in a portfolio. Nowadays however it is done with computers that automatically buy, sell, and hedge a position in real time.

While this cutting edge technology in portfolio management is cool, it can lead to massive unattended sell offs. The largest one happened on January 19th, 1988. In one day the world’s markets lost between 20-50% due to primitive algorithmic pricing of options. (source)

In 1988 the investing world was just starting to use computers to price in total risk. Many hedge fund managers at the time did not know how to operate computers as they were from the bygone era of stock ticker charting. (If interested I wrote up an article that goes over how stocks were traded before computers)

Because of this many portfolios had auto priced their total risk. When a couple variables impacted the global market there was a massive order imbalance to the sell side. When the dust had settled the world’s economy crashed by around 30% in a couple of minutes.

Flash Crash of 2010

In 2010 the U.S stock market lost over a trillion dollars in valuation in about 36 minutes. This was because of a group of risk predicting algorithms setting each other off in the fund world. (source)

Since the late 90’s the hedge fund world was using high frequency trading to scalp a couple percentage points out of the spread on a stock. The problem is that overtime everyone started to use the same methodology because it was so profitable.

Because everyone was using the same methodology the risk variables in each portfolio were the same. In 2010 the perfect storm happened where several major funds automatically sold their positions for a loss at the same time. The massive sell off was caused by one single trader who built his own algorithm in an attempt to manipulate buy and sell orders. (source)

When this traders algorithm posted false orders and deleted them before the funds algorithm could react it caused the fund to liquidate their assets. This was because the funds algorithms saw an impending crash. What happened next was a snowball effect where several funds sold for a loss causing the market to plummet in a half hour.

Why Is this Important For Predicting Future Market Crashes?

This is important because in order to predict a future stock market crash we need to understand one thing. Now markets move significantly faster than previously. In 1929 the market took 3 months to crash, in 1988 it only took 3 hours, in 2010 it only took 36 minutes.

This means that any future stock market crash is going to happen fast. Algorithms will automatically liquidate the position which will cause a snowball effect that will plummet the market price.

Simply put, the market moves faster now than ever before. Both to the upside, and to the downside.

Combining Everything Predict A Future Stock Market Crash

Let’s summarize everything we know about stock market crashes.

We live in an industrial economy whose value is propped up by three variables; innovation, credit, and consumption. These variables have to work in cohesion with each other, when one starts to dominate the market (innovation in 1932, credit in 2008, consumption in 2020) then we get a crash. Further, these crashes are happening faster with the advent of computer algorithms.

Looking forward then we need to watch the stock market for an imbalance in these variables. For example, if the stock market starts to see too much credit being consumed by the population without innovation to drive consumption then we will get a crash. Likewise if we see innovation consumption drop drastically then the market will crash due to lack of innovation (demand).

Several hedge funds have already started implementing this paradigm to manage risk in global portfolios. They use complex arbitrage strategies to maximize return while minimizing risk. It might seem hard at first but you could easily replicate these methodologies and portfolios once you know what to look for.

Conclusion

There you have it. An article that goes over the nuts and bolts of predicting stock market crashes. I have provided sources to back up the research, they are all good reads so I recommend checking them out when you get the chance.

Here at Chronohistoria I teach people how to generate above average market returns (alpha). I routinely publish articles that go over investment research, methodologies, and tips/tricks of the trade. Feel free to sign up for the free newsletter to remain up to date on everything investing.

Further, you can check out some of the other articles below.

-

How Long Does a Short Squeeze Last? (3 Answers)

What is the time frame for you short squeeze? Well here is everything you will ever need to know to determine how long it will last.

-

Why You Still Own a Stock After It’s Delisted and How to Sell It

Do you still own a stock after its delisted? How do you sell it? Don’t worry the stock is still worth money and here is how to sell.

-

Can You Make 1% A Day in the Stock Market? (3 Steps)

Making 1% a day in the stock market is hard but defiantly doable. Here are 3 simple steps to helping you achieve this return.

Until we meet again, I wish you the best of luck in your investment journey.

Sincerely,