There are two types of investors in the world. Those who are good at what they do multiply their capital, and those who are bad and ‘donate’ their capital to the market. This article is going to show you how you can make sure that you are a good investor who makes money, and not a bad investor who only loses money.

There are only 3 main differences that separate a good investor from a bad investor. They are risk management, diversification, and long term thinking. Bad investors will not factor in these differences when looking at an investment and as such will lose money. However a good investor who manages their risk, diversifies their holdings, and plans for the long term will always come out on top.

Here at Chronohistoria I teach people how to generate above normal market returns (Alpha) in our portfolios. I publish articles that research individual stocks as well as provide helpful tips/tricks of the trade. I have a free newsletter if you want to keep up to date on everything.

Let’s jump right into the 3 main differences between a good and bad investor.

Main Difference 1: Risk Management

The Good Investor

Risk management is one of the main differences that separate a good investor from a bad investor. This is because a good investor can recognize when an investment is too risky to add to their portfolio. They will look at the financial documents, sector reports, and the executive team of a company before pulling the trigger on an investment.

Because of this good investors will know what the likelihood of them losing money on an investment will be long before they actually invest. Further, a good investor will practice hedging their position so that they are always gaining in the market.

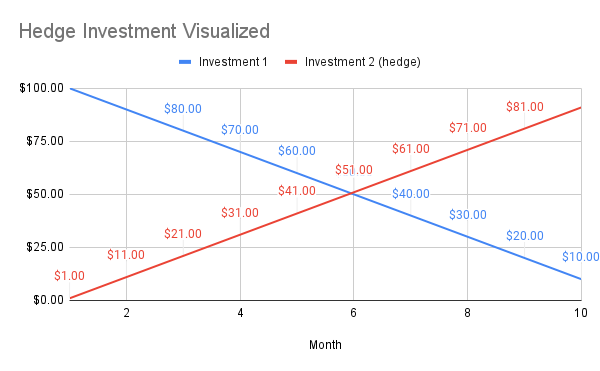

A hedge is essentially a bet against your position taken out so that if your primary investment starts losing value your hedge will start to increase in value. Here is a chart demonstrating a theoretical hedge.

In the above image a good investor will take out two investments at the same time. The blue line would be their primary investment and the red line represents the good investors hedge.

What happens is that if the primary investment (blue) starts to decline in value then the red line (hedge) will increase in value. As we can see this means that even if the good investor is wrong, they will still come out on top. This is the power of risk management.

If you want to know more about hedging then I wrote an entire article on the concept. You can check it out by clicking this link. (click here)

The good investor will always come out on top because they understand and practice risk management in their portfolio. Hedging is only one of the many tools to practice risk management. Every year new academic articles are published on theoretical strategies to lower risk in investment portfolios.

If you’re interested here is a pretty cool academic article on using algorithms to minimize risk exposure in portfolios. (Click here)

The Bad Investor

The bad investor on the other hand will simply throw their money at the screen and pray that they will make money in the long run. A bad investor is more likely to fall into pump and dump schemes or into a liquidity trap making them a bag holder.

Generally, the concept of risk management for the average retail trader is a foreign concept. The bad investor will chase returns until they have no capital left to invest with. Scorned the bad investor will then lambast the markets thinking that they are inherently unfair.

Learning risk management is actually a pretty easy thing to do. I promise you that if you spend as little as an hour learning the starter techniques you will instantly start to see a higher ROI at the end of the year. Hedging is probably one of, if not the easiest ways to provide risk management.

Main Difference 2: Diversification

The Good Investor

The good investor will hold a multitude of stocks and assets in their portfolio. Their investment portfolio might comprise around 20-30 good stocks centered around one sector or investment thesis.

Perhaps the good investor thinks that solar cell companies are going to experience rapid growth over the next 20 years. Instead of just investing in one or two companies the good investor will spread out their total investment across 20-40 good stock picks.

Nobody can accurately predict the stock market, but we can predict macro movements. The good investor will simply give their portfolio the best opportunity to grow by having a multitude of assets instead of just one.

In fact the general size of a good investor’s portfolio is around 15-20 stocks according to the surveyed average. Having over 20 stocks in your portfolio typically means you will spend countless hours researching stocks. Having under 20 stocks means that you might not be diversified enough. (Source)

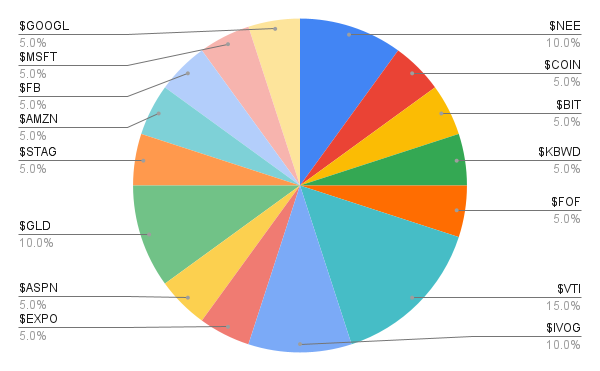

For example, here is an internal portfolio of 15 stocks we have been running here at Chronohistoria. It is based around the U.S market and has the potential to have around 20-25% growth per year while having increased risk. We hedge the portfolio with GLD as its inverse the U.S market.

The portfolio is called the growth centered portfolio. It has a monthly dividend through several stocks such as FOF, KWBD, STAG, and BIT. Also it has exposure to large cap through GOOGL,MSFT,FB,AMZN,IVOG,VTI, and NEE. Further, through ASPN, EXPO, COIN, and STAG there is large growth potential.

The 10% allocation to GLD is a hedge. The good investor can actively manage this part and buy/sell at strategic moments to maximize returns and lower risk.

A good investor will have a similar portfolio that will allow them to pursue their financial goals while also managing risk.

The Bad Investor

A bad investor will be all in on typically one or two stocks/assets. They will have 100% exposure to a certain asset class and on top of this typically be trading/investing on margin. This means that the bad investor at the end of the year will owe money to their broker.

Bad investors also pursue the latest stock hype and pumps. Sometimes this works out but a majority of the time it does not. A prime example of this would be the GME short squeeze that happened in January of 2021.

As we can see from the above image GME shot up from $40 to a huge $500 in a matter of two weeks. This massive surge in volatility and price was caused by retail traders pumping up the stock and making shorts cover for a loss.

A bad investor would have chased the pump and eventual dump of GME as it shot up in price. Chances are the bad investor would have noticed a massive loss in their portfolio during this time period.

Main Difference 3: Long Term Thinking

The Good Investor

A good investor approaches investing from a long term perspective. Instead of thinking in days and weeks like the bad investor, a good investor will focus on months and years.

The good investor is more preoccupied with where their portfolio is going to be in a couple years than what’s happening in the market currently. They spend hours researching market reports and financial documents to make sure that they are on track with their investment thesis.

This pays off in the end. If you simply build a good portfolio and let it sit you will become a millionaire over time. Investing is the easiest way to build wealth hands down. It requires little to no effort and once you know what you are doing it’s a very scalable and repeatable process.

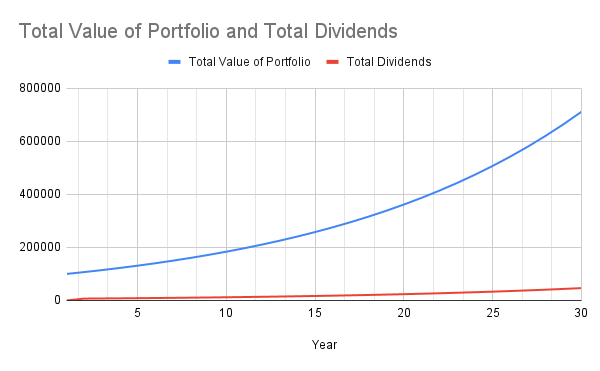

What this means is that the good investor does not care about the now, they only care about the future and how they are going to be wealthy then. For example here is a portfolio where you reinvest your dividends over a period of 30 years.

The above image demonstrates how a good investor takes advantage of compounding return to create an investment snowball. Assuming you build a $100,000 portfolio of 20 stocks that pay out a stable dividend of 5-7% and reinvest that dividend into the market. After 30 years you will come back to that portfolio and have close to a million dollars!

Further, in this theoretical portfolio your yearly dividend amount at the end of 30 years is around $70,000. This means that after 30 years you will make 70% of your initial investment every year for the rest of your life….

That is the power of investing in the hands of a good investor.

The Bad Investor

The bad investor on the other hand only thinks in the here and now. They invest with the idea of holding for a couple days and then selling for a 20-50% gain.

While they can do this a couple times it always catches up to them. That’s because in order to sustain that type of return you have to take on increasingly larger risks.

Nobody is perfect and eventually that risk will catch up with the bad investor. Then in one day they will lose 40% of their total net worth and blame the market.

Meanwhile the good investor is chugging away making their compounding return. At some point the good investor’s portfolio will dramatically eclipse the bad investors and then it’s over. The good investor has won the investing game.

Conclusion

There you have it: the 3 main differences between a good and bad investor. In reality it all comes down to learning new skills (risk management), understanding diversification, and thinking in the long term.

The stock market is an amazing machine where the whole goal is to have investors efficiently allocate capital from a bad investment to a good investment. The good investors gain a reward on this allocation of capital, while the bad investors lose their money. By reading this article you are now in the realm of the good investor, if you were not there already.

Here at Chronohistoria I teach people how to generate larger than normal market returns. I publish articles on stock research and tips/tricks of the trade. Feel free to sign up to the free newsletter, I use it to keep everyone updated on the latest stock news.

Further, you can check out some of the other articles below.

-

How Long Does a Short Squeeze Last? (3 Answers)

What is the time frame for you short squeeze? Well here is everything you will ever need to know to determine how long it will last.

-

Why You Still Own a Stock After It’s Delisted and How to Sell It

Do you still own a stock after its delisted? How do you sell it? Don’t worry the stock is still worth money and here is how to sell.

-

Can You Make 1% A Day in the Stock Market? (3 Steps)

Making 1% a day in the stock market is hard but defiantly doable. Here are 3 simple steps to helping you achieve this return.

Until next time, I wish you the best of luck in your investing journey.

Sincerely,