There is a growing sector of content moderation for online technology companies, a market that has a current valuation of $5.3 billion. Tech companies such as Facebook, Google, and Amazon have had to perform all content moderation in house, until now.

Today we are looking at a relatively unknown company called TaskUs (TASK). TASK’s whole company model is to allow the tech behemoths of the world to efficiently outsource their content moderation to TASK at a significantly cheaper rate.

This article is broken down into three sections; Fundamentals, Technicals, and I provide my Investment Thesis. Each section has sources and I put a summary at the end to save you time should you want to skip ahead.

As always if you want to remain up to date on all the stock research articles and tips/tricks then you should subscribe to the free newsletter.

Without wasting any time, let’s jump right into why TaskUs is a great investment.

Fundamentals

The fundamentals section goes over the business model, the risks, the growth strategy, and finally the finances.

The goal here is to present a whole picture of what TaskUs is all about. Their strengths and weaknesses.

At the end of the fundamentals section is a summary. Feel free to skip ahead if you are short on time. That being said I highly suggest reading the overall section so that you can get a 100% understanding.

Business Model (Source)

Whenever you upload a picture, write a sentence, or discuss something online that content is moderated. This content moderation is extremely costly to companies. A company will either have to invest millions in artificial intelligence or hire an entire workforce to review content.

In the early days of the internet this was not an issue as companies had less regulatory overhead and less overall users. Now in the 21st century content moderation has grown into a huge overhead expense for large tech companies such as Facebook, Google, Amazon, and Microsoft.

With large overhead comes opportunity and stepped TaskUs. Founded in 2008 TASK’s whole goal is to lower the overhead of content moderation for extremely large tech companies.

TASK accomplishes content moderation in two major ways. First, TASK hires around 19,000 ‘reviewers’ in the Philippines. These reviewers will read content all day to make sure that TASK’s clients are happy with the quality.

This alone has significantly cut back on the overhead of content moderation for large tech companies. However TASK has invested heavily into generating its own form of Artificial Intelligence to ultimately cut back on the amount of reviewers it needs to hire.

These two methods of content moderation have drastically cut back on the cost of content moderation for the larger tech companies who are unwilling to invest their own resources to develop the advanced algorithms.

Because of this TASK provides content moderation for 90 large tech firms in the sectors of Social Media, FinTech, HiTech, Food/Ride Delivery, Streaming, Gaming, E-Commerce, and Health Tech.

Basically TASK is well spread out across the entire emergent tech sector.

Risks (Source)

There are two major risks to TaskUs; First, is client size dominating revenue portfolio. Second, is failing to continue to innovate on artificial intelligence.

First, large clients dominate TASK’s revenue portfolio. Since TASK is still a new company in an emergent sector they are completely reliant upon around 5 key clients. These 5 clients are responsible for close to 62% of TASK’s overall revenue and a loss of a client would be huge for TASK.

The good news however is that TASK is actively branching out to smaller tech firms in need of content moderation. TASK has the necessary work force to help smaller e-commerce platforms force adequate content moderation.

This risk is a result of being a newer company in an emergent field. All ‘startups’ initially have to rely upon a few key contracts/clients. That being said, it’s a real risk. However, so long as it is cost effective for the large clients to outsource their content moderation to TASK the TASK has nothing to fear.

That leads into our second risk, failing to remain on the cutting edge of artificial intelligence. TASK has to attract and retain the necessary talent to develop cutting edge content moderation artificial technology.

As we speak TASK is seeking to buy out smaller AI companies to obtain patents and talent to build advanced algorithms. So far the executive team has successfully managed this growth. However if TASK starts to fall behind and it becomes more cost effective for the larger tech funds to spend the R&D cost to develop the necessary algorithms then TASK will start to lose revenue.

Those are the two major risks. So far TASK is actively taking the right steps and I see TASK successfully hedging against these risks in the next 3-4 months.

Growth Strategy (Source)

Since TASK’s overall business model is based around content moderation the 2020-2021 pandemic had little impact upon its operation nor its expenses.

Because of this TASK’s financial condition and market dominance rose considerably. Right now TASK is looking at potential acquisitions within the artificial intelligence sector.

Further, TASK has taken considerable steps to keep and retain vital talent such as top executives with networking capabilities. These executives have access to low cost financial loans, industry expert talent, and sit on the boards of several companies. These boards are how companies begin the process of buyouts and acquisitions.

Finally, TASK has taken considerable steps to broaden its overall content moderation client portfolio. This means taking on smaller social media companies and e-commerce stores.

Right now TASK is growing at an alarming rate and is one of the few companies in the sector that is large enough to partner with the big tech firms and buy out smaller competing companies. Overall this is a great opportunity for TASK and I am excited to see what companies they acquire.

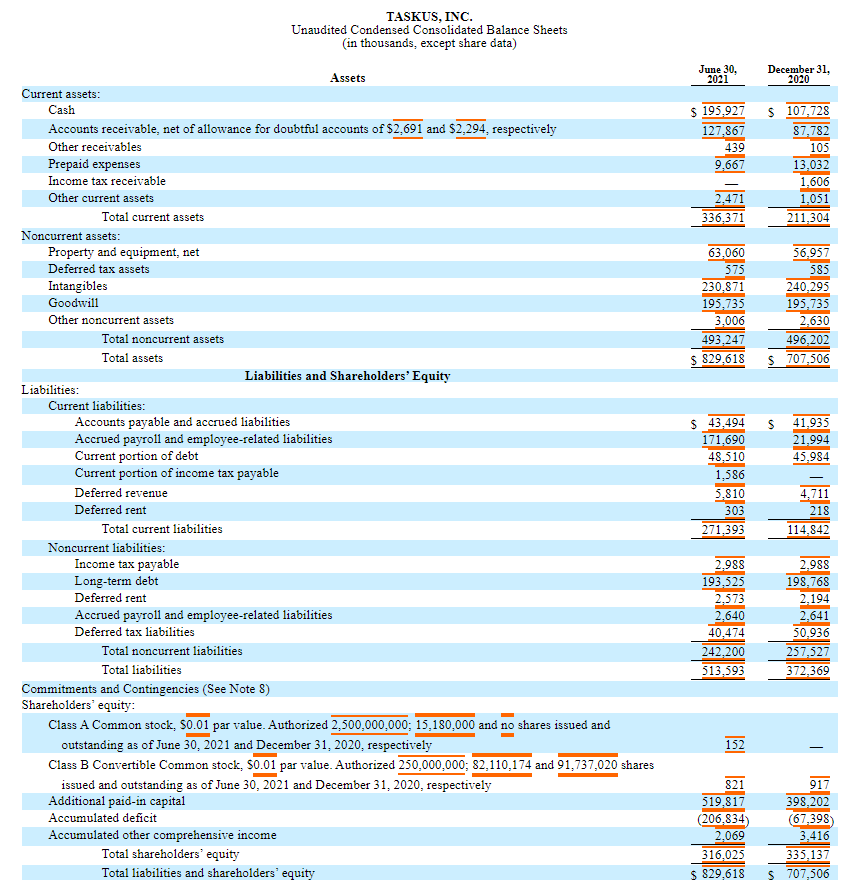

Finances (Source)

On August 10th, 2021 TASK announced their quarterly report. Within the earnings report TASK had a 46% increase in total cash and cash assets. This is a great sign for potential growth opportunities in the near future.

Adjusted net income increased by 119.6% over 2021. EBITDA also increased by 90% over the same period. This is another huge sign and indicates a ton of cash on hand for TASK going forward. (Source)

This above image of the most recent TASK quarter report (10-k) outlines the major financial bullet points. (Source)

As we can see both total current assets and total current liabilities increased. This is because TASK has drastically been upsizing and hiring new talent to manage their expanding portfolio of clients. This is a good thing. The company is not taking on increasing debt (other than salaries) and is making more money than before.

Overall the finances of TASK are currently fine. The company is experiencing some growing pains but overall there is not much to worry about. We should start to see accelerated growth over the next couple quarters.

Summary

The fundamentals of TASK are great. The business plan is solid, the risks are being actively hedged against, the growth strategy is clearly defined and easily achievable, and the finances are in a position to allow rapid expansion.

Technicals (Source)

In the technicals section we are going to go over the chart, 90/10 day average volume, and the short/float ratio.

The goal of this section is to critically evaluate how much a good investment can make in TASK and how the stock price itself will react.

Chart

The above picture is of TASK over the past 3 months. TASK is a new company that went public in the middle of 2021, as such the chart does not demonstrate that much.

However after the first earnings report we can clearly see the market begin to adequately price the stock’s economic potential into the stock. As such the stock over the past month has gained around 228%. It also has recovered from a push back and started to climb again.

90/10 Day Average Volume (Source)

The average 90 day volume on TASK is 600,000 shares traded per day. Recently however this average daily volume has almost doubled to a nice 1.08 million shares per day.

Whenever you see a 10 day average daily volume higher than the 90 day average volume (3 month) then that is a very good sign for liquidity.

If an investment has little volume then liquidity is a major concern. In fact I don’t enter investments where I am afraid that I won’t be able to liquidate efficiently enough, no matter how good an investment looks.

Fortunately for TASK, liquidity is fine. So long as you’re not investing $7 million dollars at a time.

Short/Float Ratio (Source)

The float on TASK is an extremely small 8.7 million public shares. This is because right now a majority of the shares on the market are owned by institutions.

I expect to see this float increase over time to around 40-60 million as the stock becomes more valuable. That being said, if the stock starts to experience any traction on social media then you can expect to see huge daily gains in the stock.

Right now the short percentage of the float is under 3%. This means that the chances of your investment experiencing a short squeeze is almost non-existent.

Summary of Technicals

Overall the technicals of TASK is a short section. This is because the stock is so new to the market and has to give us some more data before I can evaluate its technicals.

That being said however there are some conclusions we can draw. First, that the float is so low that any major increase in volume/publicity will skyrocket the price. Second, that the average daily volume is increasing on the stock. So long as the volume continues to increase so will the overall liquidity which will drive up value in the stock.

Investment Thesis

The investment thesis for TASK is rather simple. We know that TASK’s underlying business model is dependent upon the growth of content moderation as a whole.

Content moderation only takes place in the tech sector. The tech sector itself is expected to grow at an astounding 13% rate over the next decade. This is going to cause significant hurdles in content moderation. These hurdles are what is going to pave the way for TASK to become a huge company. (Source)

Further, the U.S national director council in 2021 published the top 10 emerging global trends that will grow at an exponential rate up until 2030. Number 5 of these emergent global trends is the power of social media to shape and influence democratic elements throughout the world. (Source)

Within the U.S alone the growing power of online content to influence cultural and social trends is rapidly expanding. The U.S Congress on January 27, 2021 published research to aid legislative debate. Within this legislative report the U.S congress addresses the ongoing need for content moderation within the United States over the foreseeable future. The conclusion; That content moderation as a service is going to continue to grow at an alarming rate. (Source)

So we have a huge demand for content moderation at an extremely high tech level. While there are plenty of smaller commercial companies offering their services, very few have the large first mover advantage that TASK does. Further, TASK has successfully demonstrated how they can obtain high net worth clients such as Uber, Facebook, Zoom, etc.

Success breeds success. Here TASK is setting itself up to be the world dominating player in content moderation.

Future Stock Price?

As always this answer is “it depends.”

In the near term (1-1.5 years) I can see TASK growing to be between $85-$95. That is a 14-24% gain, well above market average of 15-20% for the same time period.

In the long term (2-5 years) I can see TASK gaining in price to the range of $150-$170 assuming their advancements in AI content moderation continue to outpace competitors.

Further, if TASK hits above $140 I could see them start to offer a dividend to their investors. This will only further increase gain.

Conclusion

There you have it, the TASK Stock Analysis. It’s a great opportunity for the right kind of investors. As always, evaluate a position to see if it’s a good fit for your portfolio.

I would put TASK in a social media portfolio or a portfolio weighted heavily into cybersecurity. Both of those would benefit.

As always if you like content like this then feel free to subscribe to the free newsletter. Here at ChronoHistoria I put out stock research along with tips and tricks of the trade. (subscription is at top of page)

Further, you can check out some of the other articles below.

-

How Long Does a Short Squeeze Last? (3 Answers)

What is the time frame for you short squeeze? Well here is everything you will ever need to know to determine how long it will last.

-

Why You Still Own a Stock After It’s Delisted and How to Sell It

Do you still own a stock after its delisted? How do you sell it? Don’t worry the stock is still worth money and here is how to sell.

-

Can You Make 1% A Day in the Stock Market? (3 Steps)

Making 1% a day in the stock market is hard but defiantly doable. Here are 3 simple steps to helping you achieve this return.

Until we meet again, I wish you the best of luck in your investments.

Sincerely,